Microsoft Word

SECTION 1. PURPOSE This revenue procedure provides a safe harbor method under which the Internal Revenue Service will treat a fiber optic node and trunk line consisting of fiber optic cable used in a

Home / Are fiber optic junction boxes considered assets

Network equipment belongs on your balance sheet as a long-term asset, with its cost spread across future periods through depreciation rather than deducted all at once. Moreover, the useful life of fibre optic cables is affected by the intensity of their use. ermining whether all cable distribution network assets ar matic cons nt from th Commissio VOIP) pho 63(a) depends on whether the costs perty, r used intherefore disa es that, for Feder irs under § 1, while the costs of installing i r determining which customer drop costs ion 2. 2 – Is an asset that is constructed and owned by one entity, but operated by another, a leased asset? IND FAQ 6. 41, "CATV [Cable Tele-vision]-Headend," which includes assets such as towers, antennas, preamplifiers, converters, modulation equipment, and program non-duplication systems. Specifically, this revenue procedure provides two alternative safe harbor approaches for determining whether expenditures to maintain, replace, or improve cable network assets must be capitalized under § 263 (a) of the Internal Revenue Code (Code): (1) a "network asset maintenance allowance".

SECTION 1. PURPOSE This revenue procedure provides a safe harbor method under which the Internal Revenue Service will treat a fiber optic node and trunk line consisting of fiber optic cable used in a

Light Reading is the leading source of news analysis for communications industry professionals.

An intangible asset is defined in IAS 38 as an identifiable non-monetary asset without physical substance. A right to use specific wavelengths could therefore meet the definition of an

Defining Capital Expenditure Capital expenditure refers to funds used by a company to acquire, upgrade, and maintain physical assets such as buildings, technology, or equipment. In the

4. How to choose the appropriate Fiber Optic Distribution Box? When selecting a Fiber Optic Distribution Box, the following factors need to be considered:

For purposes of the new safe harbors, cable network assets specifically exclude all intangible property (with the exception of certain types of software used in the operation of the cable distribution

In the most general terms, then, eligibility of fiber optic network assets for bonus depreciation depends on the provider''s chosen accounting and

8. Conclusion In conclusion, fiber optic junction boxes are indispensable components in modern communication networks.

The revenue procedure allows a taxpayer to treat a fiber optic transfer node and trunk line consisting of fiber optic cable used in a cable distribution system as the asset for depreciation

In the most general terms, then, eligibility of fiber optic network assets for bonus depreciation depends on the provider''s chosen accounting and depreciation methods.

Less: Costs capitalized for financial statement purposes that are deducted or deferred for Federal tax purposes, other than under this network asset maintenance allowance safe harbor, such as research

I''d say yes - it''s required as part of the install - so it''s included in getting the asset ready for use.

A cable network is an expansive system of interconnected assets covering one or more geographically contiguous regions or proximate customer populations that receive cable services

The fiber optic cable (including all 120 optic fibers) and the node are the asset for depreciation purposes. The fiber optic node and cable is considered placed in service in taxable year

Capital costs in fibre deployment refer to expenses incurred to acquire, upgrade, or improve physical assets that will provide benefits over

Navigating the world of tax regulations can often feel like deciphering a foreign language, especially when it comes to understanding depreciation rules. The guidelines for fibre optic cable

have dedicated fiber optic strands and coaxial cable or dedicated wavelengths and frequencies on fiber optic strands and coaxial cables in that System, such that the Users'' signals will

That bulletin establishes a baseline for depreciation for tax purposes for fiber networks that assumes a conservative and short life for fiber assets. For

Factors such as environmental conditions and usage intensity also affect the durability of fibre optic systems. Businesses must consider these aspects when planning depreciation strategies,

Thus, a more fiber-dense region will have an Area covering fewer total square miles than one with more dispersed fiber strands. LAW AND ANALYSIS Ruling 1 Section 856 (c) (2) provides

Typically, fibre optic cables are classified as tangible property used in telecommunications. This classification is crucial as it determines the applicable depreciation scheme

The depreciation of fibre optic cables, like any other asset, affects how businesses report their financial position. Under IFRS, specific guidelines dictate how depreciation should be calculated

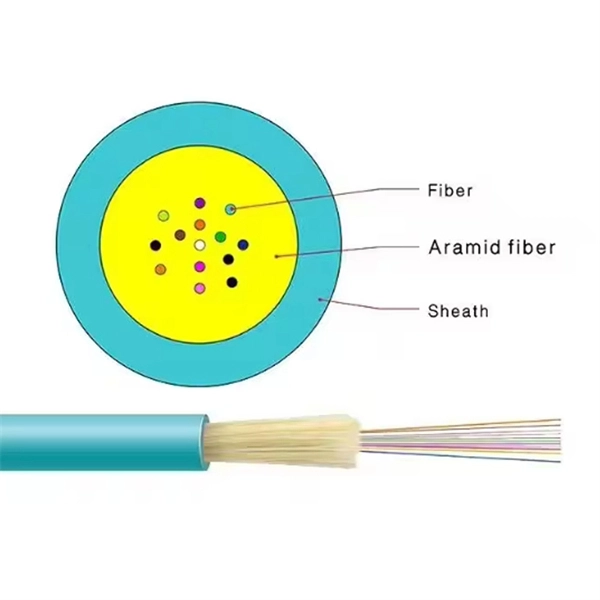

Although a fiber optic cable may contain more optic fibers than are necessary to serve a single node, all optic fibers in the unit of property are considered placed in service when the node is ready and

Thus, for example, if a taxpayer has a fiber optic cable containing 20 bundles of 6 optic fibers (120 total optic fibers) and connects 2 optic fibers to a node, the fiber optic cable (including all 120 optic fibers)

A. DAS Installations and Fiber Optic Cables Some of Taxpayer''s fiber optic cables are connected to and are associated with DAS installations, while other fiber optic cables form

Furthermore, Taxpayer will repair the fiber optic cable if it is cut or otherwise damaged, which can occur from storms, earthquakes, water incursions, fire, unauthorized digging, animal activity, etc. Taxpayer

Once you capitalize a network equipment asset, its cost gets allocated as an expense over the period it generates revenue. This is depreciation, and it moves value from the balance sheet to

Rev. Proc. 2015-12 also provides a safe harbor that the asset used for depreciation purposes encompasses the node and the fiber optic cable to that node, excluding any fiber optic

+48 22 538 72 19

ul. Postępu 14, 02-676 Warszawa, Poland